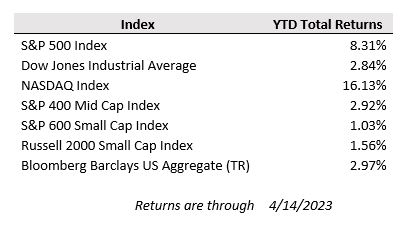

U.S. equity markets posted modest gains last week as March inflation readings came in cooler than expected and first quarter earnings season kicked off on a positive note with upside surprises from several large financial institutions. For the week, the S&P 500 gained 0.8% while the Dow Jones rose 1.2% and the Nasdaq Composite eked out a 0.3% gain. Meanwhile, despite moderating inflation readings, interest rates ticked higher last week on comments from several Federal Reserve board members who anticipate holding the Fed funds rates higher for longer than the market has priced in to ensure that price stability is restored.

While inflation remains firmly above the Fed’s 2% target, last week’s releases of March Consumer and Producer Price Index readings showed encouraging progress towards that end as the former increased just 0.1% in March while the latter fell by 0.5%. On a year-over-year basis, consumer prices grew 5.0%, down from 6.0% in February and below the consensus forecast of 5.2%. The most notable driver of the decline was a drop off in energy prices, which fell 3.5% in March, whereas core consumer prices (ex-food and energy) were a bit stickier rising 5.6% year-over-year. Producer price inflation fell even more notably, declining to a 2.7% annual growth rate in March (3.6% stripping out food and energy) from 4.9% in February. The decline in producer input costs will likely eventually pass through to consumers, at least in part as businesses look to take some of the cost improvement to increase profit margins.

Moderating inflation readings reinforce the expectations for a near-term pause in rate hikes, but market odds still tilt heavily in favor of one more 0.25% rate increase next month before the central bank hits pause. The probability of a quarter point increase in May sits at 87%, according to the CME FedWatch tool. Additionally, cooling price pressures also point to continued slowing in the demand outlook and economic growth forecasts.

On the corporate earnings front, big banks including JP Morgan Chase, Citigroup, PNC, and Wells Fargo posted solid results for the first quarter that helped soothe investor concerns on financial system stability in the wake of last month’s bank failures. Among the positive takeaways from the earnings calls, management teams noted some deposit stabilization in recent weeks, and they asserted that U.S. consumer and small business spending and credit remain resilient, though they softened somewhat as the first quarter progressed. Loan delinquency rates remain at very low levels, but banks are setting aside larger loan loss reserves with the expectation that defaults will pick up as economic growth wanes and excess stimulus savings wind down. When asked about the potential for banks to pull back on lending given deposit pressures and the uncertain economic outlook, JP Morgan CEO Jamie Dimon made it clear that he doesn’t anticipate a broad “credit crunch” that would slam the economic brakes but instead that a pullback in credit availability would be focused to certain loan categories, including segments of commercial real estate like offices and malls.

In the week ahead, first quarter earnings season will shift into a higher gear with 59 members of the S&P 500 set to report results. The S&P 500 in aggregate is expected to report a 6.7% decline in earnings in the first quarter compared to a year ago following a 3.7% year-over-year decline in the fourth quarter of 2022. Earnings growth is expected to push back into positive territory in the second half of 2023, but earnings forecasts have been gradually revised down since last June. This quarter’s results and forward-looking guidance from management teams will help determine whether future earnings expectations stabilize or continue to slide lower.