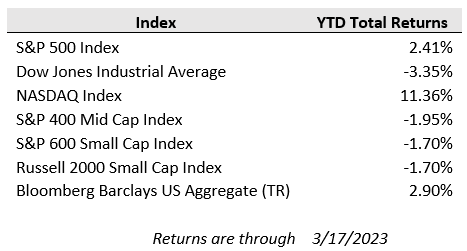

U.S. equities broadly have held up well despite tumultuous market activity triggered by the recent failures of Silicon Valley Bank and Signature Bank of New York, which sparked a selloff among financial sector stocks and ignited the strongest rally in U.S. short-term Treasury bonds in decades. For the week, the S&P 500 managed to gain 1.4% while the tech-heavy Nasdaq surged 4.4% and the Dow Jones was roughly even. Growth stocks, which are more sensitive to changes in interest rates, got a lift from tumbling bond yields despite concerns of slowing economic growth conditions. The 2-year Treasury yield, which stood at over 5% before the Silicon Valley Bank failure, fell to just 3.82% to close out the week as market participants have considerably reduced rate hike expectations in response to the pressure showing in the banking system. The financial system headlines largely overshadowed last week’s inflation readings, which showed consumer prices rising 6.0% year-over-year in February.

Over the weekend, long-time troubled Swiss-lender Credit Suisse was taken over by local rival UBS in a Swiss government-brokered deal that valued Credit Suisse at just over $3 billion compared to a $45 billion tangible book value as of the end of last year. Credit Suisse’s struggles pre-dated the current turmoil as its deposits had already fallen over 40% last year and stressed conditions accelerated the loss of remaining confidence in the lender. The UBS takeover provides an expedited outcome rather than a wait and see approach as to whether Credit Suisse could actually manage a restructuring.

Back in the U.S., the Federal Reserve has taken extraordinary measures to shore up banking system liquidity, including its deposit backstop, the Bank Term Funding Program, that allows banks to tender government bonds as collateral at par in exchange for a one-year loan. Over the past week, banks have tapped that facility for $11.9 billion in funding in addition to another $153 billion in borrowing from the Fed discount window, which was a record increase in usage. All told, including another $143 billion in funding from the FDIC to provide bridge financing to cover deposits from SVB and Signature Bank, the increase in the Fed’s balance sheet over the past week has reversed around half of the central bank’s balance sheet reduction efforts (called quantitative tightening) from the past year. While this was a notable increase, it was primarily concentrated to California and New York where the SVB and Signature Bank failures occurred, and the Fed’s liquidity backstop could provide as much as $2 trillion in total funding, according to analysts at JP Morgan.

What are the implications of all this financial system stress based on what we know today? While the situation continues to evolve quickly and there may be individual bank-specific issues yet to play out, deposit flight has slowed with bolstered confidence from regulatory support. Many U.S. regional banks are actually seeing deposit inflows given deposit movement from SVB and Signature Bank, according to S&P Capital IQ. The current liquidity crunch may have negative economic consequences, but it is much different from the credit issues that prompted the 2008 global financial crisis. In the run up to that crisis, banks took on subprime mortgages and securities collateralized by those low-quality mortgages, which were rendered next to or entirely worthless after the housing bubble popped, thereby wiping out significant equity capital. Most of the pain in today’s environment stems from bank bond portfolios of high-quality government securities that carry minimal credit risk, but their longer duration and higher interest rate sensitivity creates a mismatch against rising short-term liquidity needs. However, a 10-year Treasury purchased at the lowest point in yields in July 2020 would still be valued at over 80 cents on the dollar relative to par, and the value would gradually get pulled to par at maturity if not sold early.

One of the potential ramifications of the banking liquidity squeeze is that it may drive banks in general to further tighten lending standards and step back from higher-risk pockets of the economy as they look to maintain higher liquidity amid this backdrop of deposit uncertainty and growing public scrutiny. Slowing credit availability can throw sand in the gears of economic growth and increase the risk of failure to small and midsize businesses and highly leveraged firms that are dependent on bank financing to sustain operations. This episode in and of itself serves to tighten financial conditions much like a Fed rate hike.

The Federal Reserve will seek to take all of this into account as it plots the path forward for monetary policy with the next central bank meeting and interest rate decision occurring this week. According to the CME FedWatch Tool, markets reflect a 75% probability for a 0.25% rate hike this week and a 25% chance of no hike at all, with several rate cuts then anticipated in the back half of the year. This is a notable change from just two weeks ago where the Fed funds rate was expected to be pushed to nearly 5.75% and stay at those elevated levels throughout this year.

These bouts of uncertainty and volatility can understandably put investors on edge, but those with solid, well thought investment plans can remain confident that they are structured to weather any storm. At First Merchants Private Wealth Advisors, our investment philosophy always emphasizes a focus on the highest quality, self-sustaining companies and institutions with the knowledge that economic storms will come and capital will be pulled from places that it is not being efficiently and effectively deployed. We believe this high-quality focus is a necessity in these times of turbulence and uncertainty and that many of the businesses that we invest in on our clients’ behalf will come out stronger while other less financially stable businesses lose ground. As always, please feel free to speak one of our team of advisors if you want to discuss your investment plan.