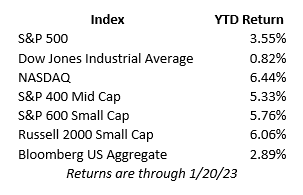

For the week of January 16th, the S&P 500 declined 0.76% and the Dow Jones declined 2.8% based on weak economic data points and signs of a slowing economy. The NASDAQ increased 0.5% behind the announcement of strong Q4 subscriber growth from Netflix. The yield on the 10-year Treasury Note briefly reached its lowest point since September and finished the week at 3.484%.

Producer Price Index (PPI), a measurement of final selling prices received by producers, fell by 0.5% in December, the largest decrease since April 2020. December retail sales fell 1.1%, manufacturing output fell 1.3%, and housing starts fell 1.4% - all falling more than the consensus estimate. These data points suggest that the US economy is slowing as interest rate increases hamper growth. Jobless claims were at their lowest level since September, confirming that the labor market is still tight. Markets have fully priced in a 25 basis point increase to the Federal Funds Rate at the upcoming FOMC meeting, but support for a 50 basis point hike by St. Louis Federal Reserve President James Bullard sent markets lower on Wednesday the 18th in fear of the Fed “overtightening.” Other Fed officials have supported a 25 basis point hike and a “higher for longer” mentality to rates, while markets are still anticipating multiple rate hikes later in the year.

Political and business leaders traveled to Davos, Switzerland for the World Economic Forum. Panels and meetings were held to discuss topics such as Russia’s invasion of Ukraine, climate change, and the threat of recession around the globe. Treasury Secretary Janet Yellen met with Chinese Vice Premier Liu He, a significant step as China continues removing COVID restrictions and re-entering the global economy. CEOs at the event were surveyed, and 75% anticipate slowing global economic growth over the next year, up from 18% that said the same at last year’s event. However, only 16% planned on firing workers, and 6% planned on cutting employee compensation, indicating that they believe any slowdown in the global economy could be short-lived.

On Thursday, January 19th, the US reached its debt ceiling of $31.4T, and the Treasury Department was forced to take “extraordinary measures” to keep the US from defaulting on debt obligations. These measures, which include halting investments in certain federal retirement funds, should allow the US to meet its debt obligations until early June. After that, changes to the debt limit or federal spending will need to be agreed upon, and lawmakers will intensify these negotiations after the US tax deadline in April. Even the threat of the US defaulting on its debt obligations would threaten the stability of the global economy.

Alphabet, Microsoft, and Amazon all announced layoffs impacting around 40,000 jobs, citing economic headwinds like inflation and interest rates. Alcoa, P&G, and Discover Financial Services also acknowledged worsening economic outlooks in their earnings announcements.

Looking to the week of January 23rd, earnings reports begin to significantly pick up with major companies in several industries reporting Q4 and FY 2022 financial results. First indications of Q4 GDP will be released by the Bureau of Economic Analysis on January 26th. Several releases related to personal consumption and income are scheduled for Friday the 27th before focus turns to the FOMC meeting beginning January 31st.