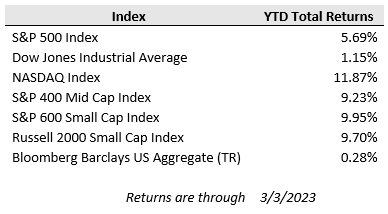

U.S. equities rallied back last Thursday and Friday to close out a volatile week in positive territory, snapping a three week stretch of consecutive losses. Rising rate hike expectations and sharp movements in long-term interest rates around key levels played a role in last week’s volatility. Equities sold off early in the week as the 10-year Treasury yield pushed above 4% to a high of 4.08% midweek before reversing course and ending the week at 3.97%. For the week, the S&P 500 and Dow Jones each rose roughly 1.9%, while the growth-heavy and more rate-sensitive Nasdaq Composite gained 2.6%.

As strong economic data continues to roll in to start the year, investors have recalibrated their outlook for the peak terminal rate to now reach at least 5.5%, with a small part of the market even considering 6%. Traders appear to have become more comfortable with the direction of the central bank.

Last week, ISM’s gauge of manufacturing activity for February rose for the first time in six months, though remained in contraction territory. On top of that, the S&P manufacturing PMI rose for February. New orders for key U.S.-manufactured capital goods increased by the most in five months in January while shipments of those so-called core goods rebounded, suggesting that business spending on equipment picked up at the start of the first quarter.

While manufacturing activity showed signs of rebounding from recent weakness, the service sector continues to grow at a robust pace, according to last week’s February ISM services report. The report showed sustained growth in demand for consumer services, healing supply chains with faster delivery times, and improving ability to source labor despite record low unemployment.

Overall, the two surveys taken together demonstrate that consumer spending remains quite strong, though is still more service-focused than goods-focused. Additionally, though there were some improvements in labor availability and price pressures, they remain far from where businesses and the Federal Reserve would like them to be, suggesting more work to be done yet on raising rates.

With that backdrop, this week’s Friday jobs report will be another crucial data point for the Federal Reserve ahead of its March FOMC meeting. Economists polled by Bloomberg forecast on average that an additional 215,000 jobs were created last month. Wage gains, an important inflation indicator, are expected to have ticked up last month with average hourly earnings up 4.8% over the last year. Fed Chair Powell will also be in the spotlight this week delivering the Fed’s monetary policy report to the Senate, the first of two days of testimony on Capitol Hill. Expect questions about the state of the economy and interest rates to dominate the conversation.