Thoughts on Recent Market Volatility

Financial markets extended their year-to-date slide this week with the S&P 500 on track for its seventh consecutive week of losses and approaching a 20% “bear market” drawdown level with the index now down over 18% below its high. While valuations have fallen sharply this year as financial assets repriced to reflect surging inflation and rising rates, U.S. corporate earnings have remained resilient with full year expectations continuing to grind higher in the face of many macro challenges. However, with inflation continuing to surprise to the upside on a series of supply-side disruptions, concerns have grown that the Federal Reserve will need to respond with a more aggressive pace of tightening of financial conditions that will quell demand to the point of economic contraction.

What caused inflation to rise in recent months?

Several factors contributed to higher inflation in recent months. For starters, lagged effects of the extraordinary policies implemented during the pandemic pushed demand for goods higher even as the global economy remained constrained. Compounding matters, the Russian invasion of Ukraine created a supply shock in many important commodities. Although this region has a modest contribution to global GDP, it is a major exporter of critical items such as agricultural products, precious metals, and industrial metals. Most importantly, this region is a major global exporter of oil and gas, and the impact of this war has been felt around the world – including at the pump here at home. Finally, China’s zero-COVID policy has taken several important cities “offline” with their lockdowns, further impacting global supply chains.

What caused the latest bout of stock market volatility?

The sell-off this week has largely been attributed to concerns on the durability of corporate margins and the ability of U.S. consumers to continue absorbing price increases in the wake of disappointing earnings reports from two ultra-large retailers, Walmart and Target. The two retail stocks have fallen roughly 20% and 29%, respectively, in the days following their quarterly results in which reported earnings fell short of expectations (though sales came in above consensus) and both management teams reduced their forward-looking guidance due to inflation pressures and changing trends among consumers. Walmart noted that lower income consumers are starting to trade down to low-cost substitutes in the face of higher prices. It is also clear that rising input costs, like freight and labor, are posing notable headwinds to corporate margins, but the reports were not all doom and gloom upon closer review.

Both Walmart and Target management teams, along with a host of other retailers who surpassed earnings expectations including TJ Maxx, Home Depot, and Lowe’s, indicated that the consumer broadly is still strong and spending, but that spending is shifting. What Walmart and Target had in common that drove the bulk of the earnings disappointments was an inventory build in durable goods (including electronics, home furnishings, and sporting goods) that have seen a sharper than expected reversion toward normal after two years of stay-at-home trends and abnormally high demand in those categories. As a result, that inventory may need to be marked down to sell in the face of falling demand, though this would also reinforce cooling inflation pressures for goods. Consumers are shifting their spending from goods to services as the pandemic controls less of our daily lives. While the S&P 500 carries much lower exposure to consumer services, the broadening and normalization of consumer behavior is a positive for the economy as a whole.

How do these economic factors impact individual companies?

Our investment philosophy (and the funds that we utilize that are reflective of our philosophy) focuses on selecting businesses demonstrating proven profitability, sustainable competitive advantages to defend that profitability, rock solid financial strength with manageable debt levels, and capable management teams that are wise stewards of shareholder capital. Even if earnings were to plateau or dip in the coming year or so, these businesses are selected for their abilities to weather economic storms, and are likely to come out stronger and more valuable on the other end.

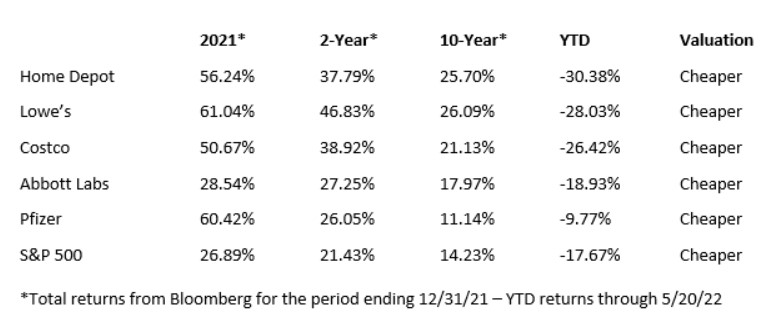

By way of example, let’s focus on the five businesses below, each of which benefitted from virus fallout. Home Depot and Lowe’s saw significant increases in their businesses as people working from home noted dingy walls, wheezing dryers, and tired backyards and decided to make improvements. Costco did well simply by its leading role in discount retailing, and an extraordinarily capable management team and employee philosophy. Abbott benefitted from its BinaxNOW testing kits and Pfizer from an extraordinary effort to evaluate and manufacture the most efficacious COVID vaccine. We’ve shown their total returns for 2021 and the 2-year and 10-year average annual returns for periods ended 12/31/2021. All but Pfizer handily beat the S&P 500 in all periods.

In the year-to-date column (through yesterday’s close) we find the inverse. All but Pfizer have fared worse than the index.

The prevailing thought regarding Home Depot, Lowe’s, Abbott, and Pfizer is that they rode the crest of a large wave now reaching the shore. Business conditions probably can’t get any better (others’ words, certainly not ours). In Costco’s case you have a discount retailer working with already very slim margins, and a sharp, quick increase in their input costs will have a magnified effect on profit margins and overall profitability, at least until they can make adjustments.

To us, these are short term conclusions that may be true, but they don’t diminish our conviction in the quality of these companies. Their business plans and philosophies are intact, employees are getting paid, and their management teams are adapting well to shifts in demand. If you have made a trip to Home Depot, Lowe’s, or Costco in the last month, you know their parking lots are full and people are four-deep at checkout lanes (more like eight deep at Costco). Selling an outstanding business based on what may or may not happen in the short term is unlikely to work in the favor of long-term investors. While the market price of a stock may swing second-by-second, the true value of a business does not.

How should investors respond?

After one of the sharpest and most severe bond market price declines in decades, many investors are understandably feeling apprehensive and skeptical on the asset class. However, there are signs of potential stabilization in long-term interest rates that may provide a light at the end of the tunnel for bond investors as the 10-year Treasury yield has bounced around in the range of 2.8% to 3.2% in recent weeks. Bond yields have lifted considerably off their pandemic lows with the Bloomberg U.S. Aggregate Bond Index yielding nearly 3.5% today after yielding barely over 1% at the end of 2020. Initial yield to maturity is a strong indicator of the annual return to be realized over the life of a bond, unless there is a default or it is sold prior to maturity. There is risk that yields rebound higher in the short-term until there are signs that inflation pressures are subsiding, but we believe the worst of the move higher in yields is behind us.

As such it may be appropriate for investors to consider taking advantage of the sharp rise in yields for bonds with maturities beyond 2 years. That may mean putting idle cash to work in short to intermediate-term bonds, or for some investors it may be advantageous to add duration to their bond portfolios, in a way that is consistent with their time horizons, using high quality investment grade bonds that would offer protection in an economic downturn.

Shifting to equity markets, which are much more sensitive to the outlook for economic growth and earnings, the turbulence that we are experiencing now may be here to stay in the short-term as market participants await clarity on the macro-economic picture. But while many seek clarity on the macro-level, we believe it is a helpful exercise to focus in at the micro-level looking at individual businesses.

At times of high volatility and uncertainty, it can feel more difficult to focus on the long-term picture and stay the course with long-term plans and objectives. In many cases, investors who make reactionary investment decisions based on a short-term outlook are turning their greatest advantage of constant liquidity and daily market pricing into their greatest disadvantage. Our team at First Merchants Private Wealth Advisors is focused on helping clients to avoid the pitfalls of investment decisions inconsistent with their time horizons and financial goals.

The market places great emphasis on expectations for the next 12 months (and many participants will shorten their perspective to the coming quarters). However, those who have a longer investment time horizon and the discipline to stick with that perspective may see a growing opportunity set of businesses selling at discounts to intrinsic values. These principles are exemplified by the legendary investor Warren Buffett, who invested a record $51 billion in equities in recent months. As always, we are here to help navigate the risks and opportunities of these uncertain times. Please don’t hesitate to reach out to your advisor with any questions or concerns.