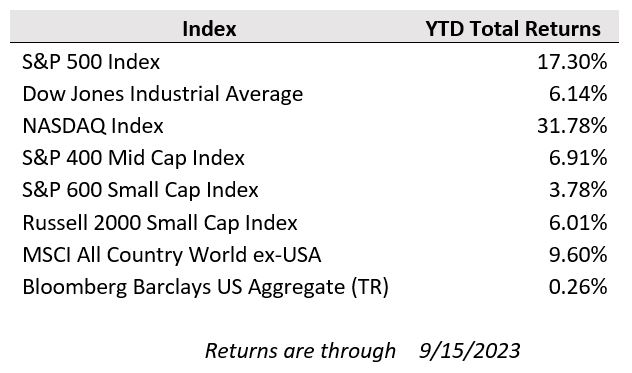

U.S. stock indexes ended last week little changed to down slightly as economic data generally came in near expectations. For the week, S&P 500 and the Dow Jones lost 0.95% and 0.33%, respectively, while the Nasdaq Composite tumbled 1.61%. Meanwhile, interest rates continued to push higher as the 10-year U.S. Treasury broke back above 4.33% last week, a 16-year high.

Domestic economic growth data has surpassed expectations by a wide margin so far in 2023 with the help of a resilient U.S. consumer and supportive fiscal policy. According to the Atlanta Fed’s GDPNow model, third quarter real GDP is on track to grow 4.9% on a seasonally adjusted annual rate, compared to a consensus economist forecast for 0% growth at the outset of the quarter. While the positive surprises have bolstered market sentiment, investors are watching several potential headwinds over the coming weeks and months that could weigh on economic momentum, including the current UAW union strike, a possible government shutdown, and the resumption of student loan payments next quarter.

United Auto Workers members walked out at three of GM, Ford and Stellantis’s more profitable plants in a targeted action that the union said could ratchet up. Though more restrained than some expected, the move marks the first time in the UAW’s 88-year-history that it is targeting all three Detroit automakers at once. Wage increases are among the sticking points in the negotiations. Executives at the three companies said they had made lucrative bargaining proposals. Economists expect the strike’s impact to be modest—if limited to a few locations and resolved quickly. Otherwise, it could pose a headwind to economic growth, curtail employment, and increase inflation. Goldman Sachs estimates that 0.1% could be shaved off third quarter GDP for each week the strike lasts.

Looking out to the fourth quarter, student loan payments are set to resume on 10/1/23, potentially putting a dent in consumer discretionary spending. Meanwhile, the odds of a government shutdown are rising as we approach the September 30th fiscal year end as Congress is running out of time to pass the 12 appropriations bills that fund government operations. The immediate impact of a shutdown would be a cut in military funding; however, key parts of the government remain exempt from cuts such as social security and homeland security. The resumption of student loan payments and a two to three week government shutdown could reduce fourth quarter GDP growth by almost 1%, according to Goldman Sachs.

On the inflation front, consumer prices rose in August at the fastest pace in more than a year due to a jump in energy costs, illustrating the potential obstacles to removing inflation out of the economy without a sharper slowdown. The consumer-price index rose 0.6% in August from the prior month, the Labor Department said Wednesday. More than half of the increase was due to higher gasoline prices. Core prices, which exclude food and energy items, rose by 0.3% last month after even lower readings in June and July. Over the past year, the headline CPI is up 3.7% and the core CPI is up 4.3%. The Producer Price Index (PPI – inflation at the production level) came in slightly better than expected, 2.2% versus 2.6%.