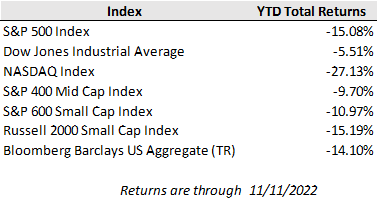

U.S. equities surged to their highest weekly gains in months in a very eventful week marked by midterm elections and a well-received October inflation report. A lower-than-expected inflation surprise spurred a sharp reversal in trends that have dominated this year as interest rates tumbled, Treasury bonds rallied, and the U.S. dollar reversed course. For the week, the S&P 500 and Dow Jones posted gains of 5.9% and 4.1%, respectively, while the beaten down Nasdaq Composite rose 8.1% as high-growth tech stocks rebounded sharply due to higher sensitivity to changes in interest rates. The 2-year and 10-year U.S. Treasury yields fell to 4.30% and 3.82% to close the week from 4.68% and 4.16% in the week prior, and the U.S. dollar notched its largest weekly fall since March 2020 with a 4.2% decline.

The October consumer price index report was a welcome reprieve to investors as downside inflation surprises have been few and far between over the past year (9 of the last 12 months of readings have surprised to the upside) and it took some steam out of the relentless rise in future rate hike expectations. Headline CPI growth fell from 8.2% year-over-year in September to 7.7% in October, coming in below the 7.9% expectation. Core CPI (excluding food & energy) also made encouraging progress falling from 6.6% year-over-year to 6.3%, and on a month-over-month basis it fell sharply from 0.6% in September to 0.3% in October. Energy and core goods (including used vehicles) continue to be large contributors to the moderation, while services generally remain an area of concern on upward pressures from shelter and other wage-driven components.

While October inflation was an encouraging data point, several Fed members have been quick to caution against overreacting to one month’s numbers in isolation as markets did back in August with a softer than expected July inflation reading. Fed Governor Chris Waller was the latest to express concerns that markets may have run too far in conflating October's inflation drop with possibility of Fed easing policy next year. He echoed Chairman Jerome Powell’s recent comments and stressed that there is a long way to go before the Fed concludes its tightening cycle even if the central bank decelerates the pace of rate increases from the recent 0.75% hike cadence.

Midterm election results also generally surprised against expectations last week with Democrats on track to retain control of the Senate and Republicans favored to take control of the House of Representatives against expectations that the GOP would gain control of both houses. A divided government would point toward greater legislative gridlock in the two years ahead as Republican control of the House likely ends the affirmative legislative phase of Biden’s presidency. This means that there is limited likelihood of any tax increases or large, progressive spending packages.

Speaking of legislation, the events of the last week in cryptocurrency markets has ignited calls for much more stringent regulatory scrutiny. Cryptocurrency markets experienced sharp losses across the board driven by the swift fall of the FTX cryptocurrency exchange from being an industry titan that had been valued at $32 billion in its most recent fundraising round earlier this year into bankruptcy last week. FTX came under pressure last week when a loss of confidence and a rush to withdraw deposits by users exposed significant liquidity issues and mismanagement of customer funds. Press articles released this weekend cited a copy of FTX's balance sheet that showed the company held just $900M in liquid assets against $9B in liabilities. The collapse has led to allegations of fraud and potential criminal misconduct probes of FTX management led by CEO Sam Bankman-Fried. Digital currencies have sustained large losses in response as it considerably undermined the confidence and trust of market participants.

In the week ahead, consumer spending will be in focus ahead of an important holiday season as October U.S. retail sales will be announced on Wednesday, and a host of large retailers are on the docket to report quarterly earnings. Investors will be paying close attention to spending trends to see if mounting price pressures and tightening financial conditions push consumers to trade-down down to cheaper goods and brands as well as to how retailers are managing through excess inventories and cost pressures.