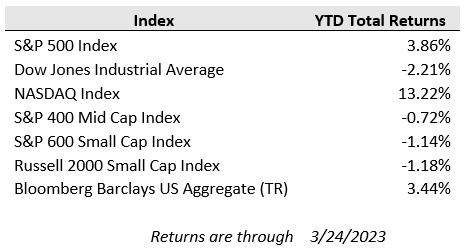

Volatility continued in the markets this past week, though stocks were able to eke out gains for the second straight week with the Dow Jones average gaining 1.2%, the S&P 500 rising 1.4%, and the Nasdaq Composite closing up 1.7%.

The ICE BofAML MOVE Index, which tracks volatility in the government bond market recently hit a 15-year high. Government bonds often experience a surge in demand when fear enters the financial markets because investors and traders often flee to the relative safety of government-backed securities. From March 10 through March 12, the 2-year Treasury yield suffered its steepest decline since October of 1987 (over the course of a 3-day trading period). The 2-year Treasury yield currently trades for roughly 3.85%, which is considerably lower than just a couple weeks ago when it was trading over 5.00%. The yield on the 10-year Treasury bond also plummeted in recent days, and currently trades for roughly 3.40%. A couple of weeks ago, the 10-year Treasury yield was trading closer to 4.00%. Bond prices are inversely correlated to yields, which means that when demand surges for government bonds, yields typically drop.

New orders for manufactured durable goods in February decreased $2.6 billion or 1.0% to $268.4 billion, down three of the last four months, the U.S. Census Bureau announced on Friday. This followed a 5.0% January decrease. Excluding the volatile transportation sector, new orders were virtually unchanged. Excluding defense, new orders decreased 0.5%. Transportation equipment, also down three of the last four months, drove the decrease, $2.6 billion or 2.8% to $89.4 billion.

Economic activity in the manufacturing sector contracted in February for the fourth consecutive month following a 28-month period of growth. The February Manufacturing PMI registered 47.7%, slightly higher than the 47.4% recorded in January (any reading below 50% represents a contraction compared to the previous month while a measure over 50% shows expansion). In the last two months, the Manufacturing PMI has been at its lowest levels since May 2020, when it registered 43.5%. The New Orders Index remained in contraction territory at 47% but rebounded from the figure of 42.5% recorded in January. Economic activity in the services sector expanded in February for the second consecutive month as the Services PMI registered 55.1%. The sector has grown in 32 of the last 33 months, with the lone contraction in December.

This week, the market will be digesting the Q4 final GDP, expected to come in at 0.90% year-over-year. PCE (the Fed’s preferred gauge for inflation) will also be released this week. Estimates are for a 5.1% year-over-year increase.

In the coming weeks, we expect investors to continue to focus on inflation and economic growth data as well as any additional problems in the global banking system.