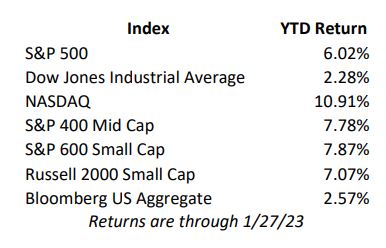

The major market averages finished higher for the week, with the Nasdaq Composite climbing 4.3%, a fourth straight week of gains, while the S&P 500 gained 2.4% and the Dow Jones average ended up 1.8%.

Pending home sales increased in December for the first time since May 2022 — following six consecutive months of declines — according to the National Association of Realtors®. The Pending Home Sales Index (PHSI) — a forward-looking indicator of home sales based on contract signings — improved 2.5% to 76.9 in December. Expectations had been for a 1.0% decline. Year-over-year, pending transactions dropped by 33.8%. All four U.S. regions saw year-over-year decreases in transactions, with the West experiencing the largest decline at 37.5%.

The Index of Leading Economic indicators fell again in December, this time by 1%, the tenth consecutive monthly decline, with the monthly declines generally worsening over time. The last seven times the index has fallen this much, even if the decline was slower, a recession followed. Leading indicators are economic series that tend to change direction ahead of shifts in the business cycle. There are 10 components of the U.S. Leading Composite Indicator published by The Conference Board. Overall economic activity is likely to turn negative in the coming quarters before picking up again later in 2023.

The Personal Consumption Expenditures (PCE) index showed that consumer prices rose 0.1% from the previous month and rose 5% on an annual basis, according to the Bureau of Labor Statistics. Core prices, which strip out the more volatile measurements of food and energy, climbed 0.3% from the previous month and 4.4% year-over-year. While both are lower and trending down from the highs last year, these prints are still the highest since 1991. Both the core and headline numbers point to inflation that is running well above the Fed's preferred 2% target. Policymakers have already approved seven straight rate hikes, pushing the federal funds rate well into restrictive territory. The central bank has signaled that it will raise rates higher than previously anticipated, though it plans to pause the increases at some point in 2023.

Real gross domestic product (GDP) increased at an annual rate of 2.9 percent in the fourth quarter of 2022, besting the 2.3% expectations according to the advance estimate released by the Bureau of Economic Analysis. In the third quarter, real GDP increased 3.2 percent. The increase in real GDP reflected increases in private inventory investment, consumer spending, federal government spending, state and local government spending, and nonresidential fixed investment that were partly offset by decreases in residential fixed investment and exports.

All eyes will be on the Fed this week, as they are anticipated to increase the Fed funds rate another 25-basis points to take the target federal funds rate to 4.50% to 4.75%. The consensus view is that the Fed will continue with its tightening policy and signal more rate hikes are still in the mix.