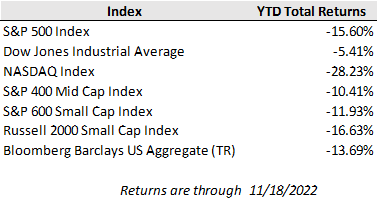

Stocks turned lower last week as the recent sharp market rally driven by cooler October inflation data began to lose some steam after Fed officials poured cold water on the idea that the central bank may be near pausing rate hikes. Specifically, St. Louis Federal Reserve President Jim Bullard said the central bank's appropriate target for the federal funds rate could end up as high as 7%, well above the current 3.75%-4% range. The Boston Fed's Susan Collins followed up on Friday that she was not ruling out a 75-basis point rate hike in December. For the week, the Dow Jones average ended even, while the S&P 500 fell 0.7% and the Nasdaq Composite dropped 1.6%.

Meanwhile, oil prices tumbled roughly 10% last week and are under further pressure this week on mounting global economic growth concerns, exacerbated by recent Covid news out of China, which this weekend announced its first three Covid-related deaths since the Shanghai lockdowns back in May. New cases also rose to their highest levels since April with 27k new cases on Sunday. China had recently shifted towards a relaxation of their zero-Covid policies, but there are concerns that the recent rise in cases will cause officials to rethink those plans.

While economic growth concerns are broadening, the U.S. consumer is still showing resilience as evidenced by October’s U.S. retail sales numbers, which grew 1.3% over September, beating expectations for a 1.0% increase. Quarterly reports from major retailers last week generally confirmed healthy consumer spending as Walmart, Home Depot, and Lowe’s all posted higher than expected sales growth. However, strong October sales could also indicate a pull forward in holiday shopping as retailers started discounting early this year to clear out excess inventory. Along this line, Target struck a more cautious tone on its earnings call last week, stating that shoppers have pulled back in recent weeks on discretionary goods spending.

The fallout within cryptocurrency markets has continued as new information has come to light following the failure of the FTX cryptocurrency exchange. Crypto broker Genesis paused withdrawals, raising concerns among the many companies that user it to provide their crypto customers with yield. FTX is not your typical failed company. John Ray, who handled Enron’s bankruptcy and was named chief executive of FTX when it filed for Chapter 11 protection, said that he had found very little documentation of finances and that what did exist couldn’t be trusted. He told the Bankruptcy Court that he had never seen a situation as chaotic as FTX. More than 100 affiliated companies are filing for bankruptcy with FTX. A million or more creditors could line up. The situation is so dire that FTX has already said it doesn’t know who its top creditors are or where many assets can be found.

Investors face a holiday-shortened this week that could see potentially lighter trading volume. The highlight of the economic calendar looks to be the release of the minutes of the last FOMC meeting on Wednesday. Retail earnings results will also continue to roll in with Best Buy, Dollar Tree, and DICK's Sporting Goods some of the headliners. Watch for guidance updates with plenty of uncertainty in the air. On Wall Street, Citi Bank U.S. equity strategist Scott Chronert has already warned of a "consumer-led recession" in 2023, which could be amplified even more if the retail heavyweights continue to pull in expectations. On the global stage, the World Cup will surely lift spirits and break hearts, even though the economic impact may be minimal.

From everyone at First Merchants Private Wealth Advisors, we wish a Happy Thanksgiving and safe travels to you and yours.